Is Mold Remediation Covered By Insurance In Tampa Bay?

Key Takeaways

- Homeowners insurance typically covers mold remediation only when it results from a covered peril like sudden pipe bursts or appliance leaks.

- Standard policies exclude mold damage from maintenance issues, flooding, or long-term moisture problems.

- Many insurers cap mold coverage at $5,000-$10,000, which may be insufficient for extensive remediation projects.

- Adding specific mold endorsements to your policy can provide additional protection beyond standard coverage limits.

- Proper documentation, quick response to water incidents, and regular home maintenance are crucial for successful mold-related claims.

Discovering mold in your home can trigger immediate concerns about health risks, structural damage, and the potentially staggering costs of remediation. When facing this unwelcome intruder, one of the first questions homeowners ask is whether their insurance will help shoulder the financial burden of mold removal and repairs. The answer isn’t as straightforward as you might hope, with coverage depending on several critical factors including the cause of the mold and the specifics of your policy.

What Every Homeowner Should Know About Mold and Insurance

Mold remediation exists in a gray area for many insurance policies. Unlike clear-cut perils such as fire or theft, mold damage involves investigating root causes, preventability factors, and policy-specific exclusions. Understanding these nuances before you discover fuzzy patches spreading across your walls or ceiling can save you significant stress and financial hardship down the road.

The High Cost of Mold Damage

Professional mold remediation isn’t cheap—costs typically range from $1,500 to $10,000, with severe infestations potentially exceeding $30,000. These expenses include not just removal of the mold itself, but often replacement of affected building materials, addressing the underlying moisture issues, and in some cases, temporary relocation during the remediation process. Without insurance coverage, these costs fall entirely on the homeowner, making proper coverage understanding essential for financial protection.

Most Standard Policies Have Limitations

Standard homeowners insurance policies approach mold with caution and limitations. While they don’t typically exclude all mold damage outright, they often contain specific language limiting coverage to certain scenarios. Many policies include mold exclusions with exceptions, meaning they exclude mold generally but provide coverage when it results from specific covered water damage events. Others may place strict sublimits on mold claims—sometimes as low as $5,000—regardless of the total coverage limits for other types of damage.

The insurance industry’s cautious approach to mold stems from the “mold crisis” of the early 2000s, when insurers faced billions in claims related to toxic mold. Following this period, many companies rewrote policies to limit their exposure to mold-related losses, creating the complex coverage landscape we navigate today.

When Coverage Is Most Likely

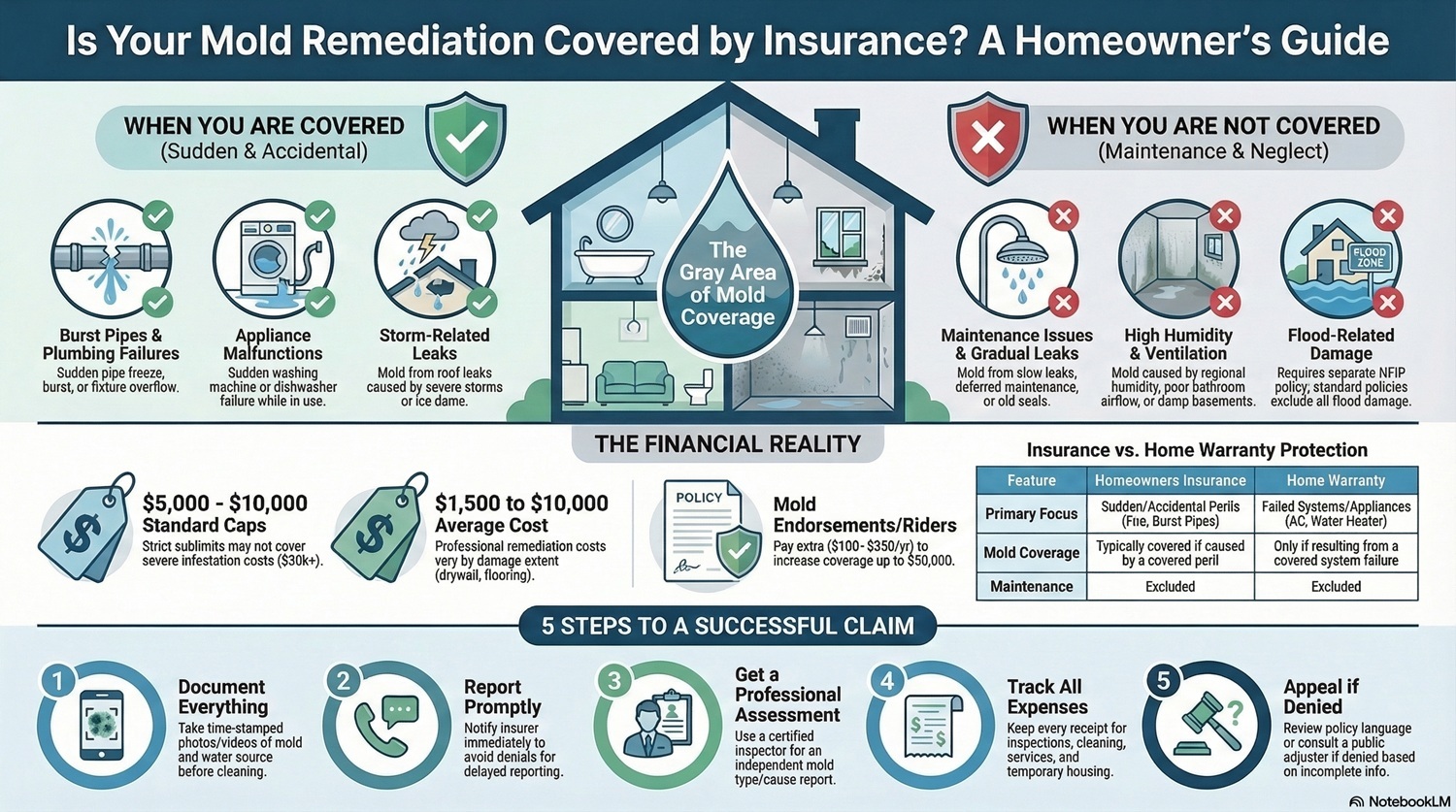

Your homeowners insurance is most likely to cover mold remediation when the growth results from a “sudden and accidental” water event that’s already covered by your policy. For instance, if your dishwasher suddenly malfunctions, flooding your kitchen and causing mold to develop in the cabinetry and drywall, this scenario typically falls under covered water damage. Similarly, mold resulting from extinguishing a house fire, burst pipes during freezing weather, or a roof leak following a severe storm would generally qualify for coverage under standard policies.

The key factor insurance companies evaluate is whether the water event was sudden and unexpected rather than gradual or preventable through normal maintenance. This distinction forms the critical dividing line between covered and non-covered mold claims in most insurance policies.

When Insurance Will Cover Mold Remediation

Navigating mold coverage requires understanding the specific circumstances where your policy will likely provide protection. While individual policies vary, certain scenarios consistently qualify for coverage across most standard homeowners insurance plans.

Mold Resulting from Covered Water Damage

When mold develops as a direct result of water damage that’s already covered under your policy, remediation costs typically receive coverage. This includes scenarios like water damage from burst pipes during winter freezes, sudden appliance failures that release water into your home, or accidental overflows from plumbing fixtures. The critical factor here is that the water event itself must qualify as a covered peril under your existing policy before the resulting mold damage can be considered.

Sudden and Accidental Events

Insurance companies distinguish between gradual damage and sudden, accidental events when evaluating mold claims. If water damage occurs suddenly—such as from a washing machine hose that ruptures while you’re at work—and mold develops before you can reasonably discover and address the issue, your insurance will likely cover remediation. The key factors are the unexpected nature of the water intrusion and your prompt action once discovering the problem. Remember that most policies require you to take immediate reasonable steps to prevent further damage, including drying out affected areas to prevent mold growth.

Examples of Covered Scenarios

Understanding specific examples helps clarify when mold remediation typically receives coverage. If an ice dam causes water to back up under your shingles and leak into your attic, resulting in mold growth, most policies would cover this damage because the initial water intrusion resulted from a covered weather event. Similarly, if your water heater suddenly ruptures, flooding your basement and causing hidden mold behind walls, remediation would generally be covered because the initiating event was sudden and accidental.

Real-World Example: After a severe winter storm, the Smith family’s upstairs pipe burst while they were away on vacation. Water saturated the ceiling and walls for several days before discovery. Upon return, they found extensive mold growth throughout the affected areas. Their insurance covered both water damage repairs and the complete mold remediation because the incident stemmed from a covered peril (sudden pipe burst due to freezing) and the family couldn’t have reasonably prevented the mold growth given their absence.

Another common covered scenario involves washing machine or dishwasher malfunctions that release water behind or under appliances, creating hidden moisture that leads to mold before detection. Since the water release was sudden and not due to negligence, most policies cover both the initial water damage and subsequent mold remediation.

Common Situations Where Mold Isn’t Covered

While certain scenarios qualify for mold remediation coverage, many common situations fall outside the protection of standard policies. Understanding these exclusions helps homeowners recognize their responsibility in preventing mold growth and maintaining appropriate home moisture levels.

Maintenance Issues and Neglect

Insurance companies expect homeowners to perform regular maintenance that prevents mold growth. Any mold resulting from deferred maintenance or neglect typically receives no coverage. For example, if your shower has been leaking for months and eventually causes mold in the bathroom walls, insurers will likely deny the claim because the problem developed gradually and could have been prevented through proper maintenance. Similarly, failing to fix a known roof leak or plumbing issue that eventually leads to mold growth constitutes neglect in the eyes of most insurance companies.

Insurers may also deny claims if they determine you didn’t take appropriate steps to mitigate damage after a water event. If your basement floods and you fail to properly dry and clean affected areas, resulting in mold growth, your insurer might cover the initial water damage but deny coverage for the subsequent mold remediation that could have been prevented.

Flood-Related Mold Damage

Standard homeowners insurance policies exclude flood damage, including any mold that develops as a result of flooding. This exclusion applies whether the flooding comes from external sources like overflowing rivers or internal sources considered flood-like, such as a sewer backup. For protection against flood-related mold damage, homeowners need separate flood insurance, typically through the National Flood Insurance Program (NFIP) or private flood insurance carriers. Even with flood insurance, policies often limit mold coverage if the homeowner doesn’t take reasonable steps to prevent mold growth after floodwaters recede.

Long-Term Moisture Problems

Mold resulting from long-term, persistent moisture issues rarely qualifies for insurance coverage. This includes ongoing humidity problems, repeated condensation issues, or chronic small leaks that create conditions favorable for mold growth over time. Insurance companies view these situations as maintenance issues rather than sudden, accidental events. Remediation for mold growing in chronically damp basements, around improperly sealed windows, or in poorly ventilated bathrooms typically falls entirely on the homeowner’s shoulders.

High Humidity and Poor Ventilation

Homes in humid climates face increased mold risks, but insurance policies don’t cover mold resulting simply from regional climate conditions or inadequate home ventilation. If your bathroom lacks proper ventilation and develops mold from shower steam, or if your basement grows mold due to natural humidity without proper dehumidification, these scenarios fall outside insurance coverage parameters. Insurance companies expect homeowners to maintain appropriate humidity levels and ventilation as part of routine home maintenance, especially in moisture-prone areas of the home.

Insurance Policy Options for Mold Coverage

Understanding the limitations of standard homeowners insurance policies is the first step toward securing adequate mold protection. While basic coverage often falls short, several policy options can enhance your mold remediation safety net.

Insurers recognize that mold represents a significant concern for many homeowners, leading to the development of specialized coverage options that address these gaps. Exploring these additional protections, such as those discussed in Progressive’s guide on mold coverage, before you need them can save thousands in potential out-of-pocket expenses.

Standard Policy Limitations

Most homeowners are surprised to discover their standard policies typically cap mold damage coverage between $5,000 and $10,000—far below what extensive remediation might cost. Some policies go even further, limiting coverage to as little as $1,000 for mold-related claims. These caps apply even when the mold results from a covered peril, creating a significant potential financial exposure for homeowners facing serious mold issues. Review your policy’s declaration page and exclusions section carefully to identify any mold-specific limitations before you need to file a claim.

Mold Endorsements and Riders

Many insurance companies offer mold coverage endorsements or riders that can be added to your standard policy for additional premium costs. These add-ons typically increase your mold coverage limits beyond the standard caps, with some providing up to $50,000 in mold remediation protection. While these endorsements increase your premium costs—usually between $100 and $350 annually depending on your location and home characteristics—they provide substantial additional protection for homes in humid climates or with higher mold risk factors. Some endorsements not only raise coverage limits but also broaden the circumstances under which mold remediation receives coverage.

Coverage Caps and Sublimits

When shopping for enhanced mold protection, pay close attention to how coverage caps and sublimits are structured. Some policies offer what appears to be comprehensive mold coverage but contain sublimits that significantly restrict actual protection. For example, a policy might advertise $25,000 in mold coverage but limit payouts to $5,000 for remediation of certain building components or exclude coverage for personal belongings damaged by mold. Understanding these nuances helps ensure you select coverage that addresses your specific concerns rather than leaving critical gaps in protection. For more information, you can read about homeowners insurance covering mold.

Companies That Offer Better Mold Protection

Several insurance carriers have developed reputations for more comprehensive mold coverage options. Companies like Openly Insurance offer high-value home insurance policies with more generous mold remediation provisions than standard market offerings. Premium carriers often provide more flexible mold coverage options, particularly for well-maintained homes with updated plumbing and climate control systems. Working with an independent insurance agent familiar with multiple carriers’ mold coverage provisions can help identify the best options for your specific home and risk profile.

How to File a Successful Mold Claim

When facing mold damage potentially covered by your insurance, proper claim filing procedures significantly impact your likelihood of approval. Following these steps helps establish the sudden and accidental nature of the damage and demonstrate your due diligence as a homeowner.

1. Document Everything Immediately

The moment you discover potential mold damage, begin comprehensive documentation. Take detailed photographs and videos of the affected areas, showing both the mold growth and any related water damage. Capture time-stamped images before attempting any cleanup, as these provide critical evidence of the damage extent. Document when and how you discovered the issue, including any related water incidents that might have caused the mold. This timeline helps establish the sudden nature of the damage rather than a long-term maintenance issue, significantly improving your chances of claim approval.

2. Report the Damage Promptly

Contact your insurance company immediately after discovering mold, even if you’re unsure whether it will be covered. Many policies include specific timeframes for reporting potential claims, and delayed reporting can become grounds for denial. During this initial contact, ask about specific documentation requirements and whether you should wait for an adjuster before beginning remediation efforts. Request a claim number and direct contact information for your assigned claims representative to facilitate ongoing communication throughout the process.

3. Get Professional Assessment

Hiring a certified mold inspector provides crucial documentation for your insurance claim. These professionals can determine the mold type, extent of contamination, and likely cause—all factors insurance companies evaluate when processing claims. The inspection report serves as independent verification of your claim details and often identifies hidden damage not visible during initial assessment. Many insurers prefer or even require assessment from certified professionals rather than relying solely on homeowner-provided documentation.

4. Keep All Receipts and Estimates

Maintain meticulous records of all expenses related to the mold damage, including inspection costs, temporary repairs, cleaning supplies, and professional remediation services. Request detailed written estimates from multiple remediation companies, as these help establish the reasonable cost of necessary repairs. If temporary relocation becomes necessary during remediation, track all associated expenses including hotel costs, meals, and additional transportation expenses. These records form the foundation of your claim’s value determination and ensure you receive appropriate compensation for covered losses.

5. Appeal Denied Claims When Appropriate

If your initial claim faces denial, carefully review the rejection explanation against your policy language. Many denials result from miscommunication or incomplete information rather than legitimate coverage exclusions. Most insurance companies have formal appeals processes allowing you to submit additional documentation or clarification addressing their specific concerns. Consider consulting with a public adjuster or attorney specializing in insurance claims if facing a significant denial, as these professionals can identify overlooked policy provisions supporting coverage and navigate complex appeal procedures on your behalf.

Smart Prevention Steps That Help Maintain Coverage

Insurance companies increasingly evaluate homeowners’ preventive measures when determining mold claim eligibility. Implementing proper prevention not only reduces your risk of mold problems but also strengthens your position if you need to file a claim.

Regular Home Maintenance That Insurers Expect

Insurance providers expect homeowners to perform reasonable maintenance that prevents mold growth. This includes regularly inspecting plumbing connections for leaks, checking and cleaning gutters and downspouts, and ensuring proper drainage away from your home’s foundation. Promptly repair roof leaks, window seals, and any water intrusion points to demonstrate proper home maintenance. Document these regular maintenance activities, as this evidence can prove invaluable if you later need to demonstrate you’ve fulfilled your responsibility to prevent foreseeable mold issues.

Humidity Control and Ventilation

Maintaining appropriate indoor humidity levels between 30-50% significantly reduces mold risk and demonstrates proactive home management to insurers. Install and use bathroom and kitchen exhaust fans that vent to the exterior rather than into attics or wall cavities where moisture can accumulate. Consider using dehumidifiers in naturally damp areas like basements, especially in humid climates. Some insurers offer premium discounts for homes with whole-house dehumidification systems or smart humidity monitoring devices that help prevent conditions conducive to mold growth.

Quick Response to Water Leaks

Immediate response to water intrusion represents the single most effective way to prevent mold growth and maintain insurance coverage eligibility. When water events occur, thoroughly dry affected areas within 24-48 hours—the typical timeframe before mold begins developing in damp materials. Consider investing in water leak detection systems that automatically shut off water supply when leaks are detected, as these devices can prevent significant damage when you’re away from home. Document your response efforts with photos and receipts for equipment rentals or professional services, as this documentation demonstrates your diligence in preventing secondary mold damage.

Modern smart home water monitoring systems can detect microscopic leaks before visible damage occurs and provide alerts to your smartphone, allowing immediate response even when you’re away from home. Many insurance companies now offer policy discounts for homes equipped with these monitoring systems, recognizing their effectiveness in preventing water damage and subsequent mold growth.

Protection Beyond Insurance

Given the limitations of standard insurance policies, prudent homeowners should explore additional protection mechanisms that complement their insurance coverage. These alternative protections can fill crucial gaps, particularly for homes with higher mold risk factors like age, climate conditions, or construction methods.

Creating a comprehensive mold protection strategy often requires layering multiple protection mechanisms rather than relying solely on homeowners insurance. This multi-faceted approach provides more complete financial protection against the full spectrum of potential mold scenarios.

Home Warranties and Mold

Home warranty programs sometimes provide limited coverage for mold remediation when it results from covered system or appliance failures. For instance, if your covered water heater leaks and causes mold damage, some warranty programs will cover both the appliance repair and resulting property damage including mold remediation. However, warranty coverage typically applies only when the mold directly results from the failure of a covered component rather than general moisture issues or structural problems.

When evaluating home warranty options, look specifically for programs that include secondary damage coverage rather than limiting protection to just the failed system or appliance itself. Premium warranty programs offering “consequential damage” provisions provide the strongest protection for mold resulting from system failures.

Coverage Comparison: Insurance vs. Warranty

Homeowners Insurance: Typically covers mold from sudden, accidental water events like burst pipes or appliance failures. Excludes maintenance issues.

Home Warranty: May cover mold resulting directly from failure of covered systems/appliances. Focus on the failed component with limited property damage coverage.

Best Protection: Combining comprehensive homeowners insurance with mold endorsements and a warranty with consequential damage coverage provides the most complete protection.

Some home warranty companies have begun offering specific mold coverage riders that extend protection beyond standard warranty limitations, though these typically come with significant additional costs and coverage caps similar to insurance policies.

Specialized Mold Insurance Products

Several insurance providers now offer stand-alone mold insurance policies designed specifically to address the coverage gaps in standard homeowners insurance. These specialized policies typically provide higher coverage limits for mold remediation regardless of cause, often covering scenarios excluded from standard policies such as long-term humidity issues or minor ongoing leaks. While considerably more expensive than standard policy endorsements, these specialized products provide comprehensive protection particularly valuable for older homes, properties in humid climates, or those with previous mold issues that might make standard coverage difficult to obtain.

Contractor Guarantees

Professional remediation companies often provide workmanship guarantees that protect against mold recurrence following their treatment. These guarantees typically cover specified periods (often 1-5 years) and provide retreatment at no additional cost if mold returns to previously remediated areas. When selecting remediation contractors, prioritize those offering robust guarantees backed by insurance or bonding to ensure they can fulfill their obligations even if the company faces financial difficulties. Some premium remediation providers offer transferable guarantees that remain valid if you sell your home, providing additional value and peace of mind for both you and potential buyers. For more information on coverage, you can explore homeowners insurance policies related to mold.

Frequently Asked Questions

Navigating the complexities of mold coverage generates numerous questions from homeowners. Below are answers to the most common inquiries, providing clarity on insurance coverage for various mold situations.

Understanding these frequently asked questions helps homeowners set realistic expectations about their coverage and take appropriate steps to maximize protection against mold-related expenses.

Does homeowners insurance cover black mold specifically?

Homeowners insurance doesn’t distinguish between mold types when determining coverage eligibility. Whether the mold is Stachybotrys chartarum (commonly known as “black mold”) or any other variety, coverage depends entirely on the cause rather than the specific mold species. The same coverage rules apply—if the mold resulted from a covered peril like sudden pipe bursts, insurance typically provides coverage up to policy limits regardless of mold type. However, the remediation costs for black mold may be higher due to its potential health hazards, possibly exceeding standard policy sublimits more quickly than other mold varieties.

If you suspect black mold specifically, document this concern when filing your claim, as it may influence remediation protocols and potentially justify more extensive coverage under certain policy provisions relating to health hazards.

How much does mold remediation typically cost?

Mold remediation costs vary dramatically based on the extent of infestation, affected materials, and your geographic location. Minor remediation limited to a single room typically ranges from $1,500 to $4,000, while moderate damage affecting multiple areas or requiring significant material replacement can range from $4,000 to $12,000. Severe infestations involving structural components or HVAC systems can exceed $30,000, especially when remediation requires removing and replacing significant portions of drywall, flooring, or other building materials. These costs often exceed standard policy sublimits for mold, highlighting the importance of additional coverage endorsements for comprehensive protection.

Can I add mold coverage to my existing policy?

Most major insurance carriers offer mold coverage endorsements that can be added to existing policies, though availability varies by state and individual property characteristics. Contact your insurance agent to inquire about specific endorsement options, coverage limits, and additional premium costs. When requesting these endorsements, be prepared for potential property inspections as insurers may want to verify your home doesn’t have existing mold issues before extending coverage. Some carriers offer tiered endorsement options with varying coverage limits and corresponding premium increases, allowing you to select protection levels aligned with your specific concerns and budget constraints.

Will insurance cover mold found during renovations?

Insurance rarely covers mold discovered during planned renovations, as these findings typically indicate long-term issues rather than sudden, accidental damage. However, if the renovation itself causes water damage that leads to new mold growth—such as a contractor accidentally breaking a water line—insurance may cover the resulting remediation. The key factors insurance companies evaluate include whether the mold existed before renovations began and whether any new water intrusion resulted from covered perils. To protect yourself during renovation projects, consider adding builder’s risk insurance that specifically includes provisions for discovered conditions and remediation requirements.

If you suspect your home might have hidden mold issues, consider professional mold inspection before beginning major renovations. This proactive approach allows you to address potential problems before they complicate your renovation timeline and budget.

Does renters insurance cover mold damage to my belongings?

- Renters insurance typically covers mold damage to personal property if it results from a covered peril, such as sudden pipe bursts or appliance leaks.

- Coverage excludes mold damage resulting from tenant negligence, high humidity, or poor ventilation.

- Most policies contain similar mold limitations and sublimits as homeowners insurance, often capping coverage at $1,000-$5,000.

- Renters insurance never covers remediation of the building structure itself—that responsibility falls to the landlord’s insurance.

- Some carriers offer personal property mold endorsements specifically for renters, providing additional protection for belongings in humid environments.

Understanding your insurance coverage for mold remediation empowers you to make informed decisions about your home’s protection. While standard policies offer limited coverage, additional endorsements and preventive measures can significantly enhance your financial security against mold-related expenses.

Remember that documentation, quick response to water events, and proper home maintenance not only prevent mold growth but also strengthen your position when filing insurance claims. When in doubt about your specific coverage, consult directly with your insurance agent to review policy details and available enhancement options.

For homeowners in humid climates or with older homes, consider comprehensive protection strategies that combine insurance coverage with preventive technologies and professional inspections. This layered approach provides the strongest defense against both the health hazards and financial impacts of household mold.

Addressing mold concerns proactively rather than reactively not only protects your home’s value but also ensures your family’s health and comfort for years to come. With proper insurance coverage and prevention strategies, you can face potential mold issues with confidence rather than financial anxiety.