Does Homeowners Insurance Cover Mold Inspection in Florida?

- Homeowners insurance in Florida may cover mold damage, but only when mold results from a sudden, covered water event — not from long-term moisture buildup or maintenance neglect.

- Mold inspection costs are rarely covered on their own — coverage typically depends on whether the inspection is part of a covered water damage claim.

- Florida’s climate makes mold one of the most common and costly home damage risks in the state, with remediation costs that can reach tens of thousands of dollars.

- Florida Peninsula Insurance offers homeowners policies with mold remediation coverage options worth reviewing before mold becomes a costly surprise.

- Most standard policies include limited mold coverage with a sub-limit — and many homeowners don’t realize how low that limit is until they’re already filing a claim.

Mold in a Florida home isn’t just a cosmetic problem — it can be a financial one, and whether your insurance policy helps pay for it depends on details most homeowners never think to check. Florida homeowners face a unique set of risks when it comes to mold. The combination of year-round humidity, frequent rain, and storm-related water intrusion makes mold growth not just possible but nearly inevitable at some point in homeownership.

Florida Mold and Insurance: The Short Answer

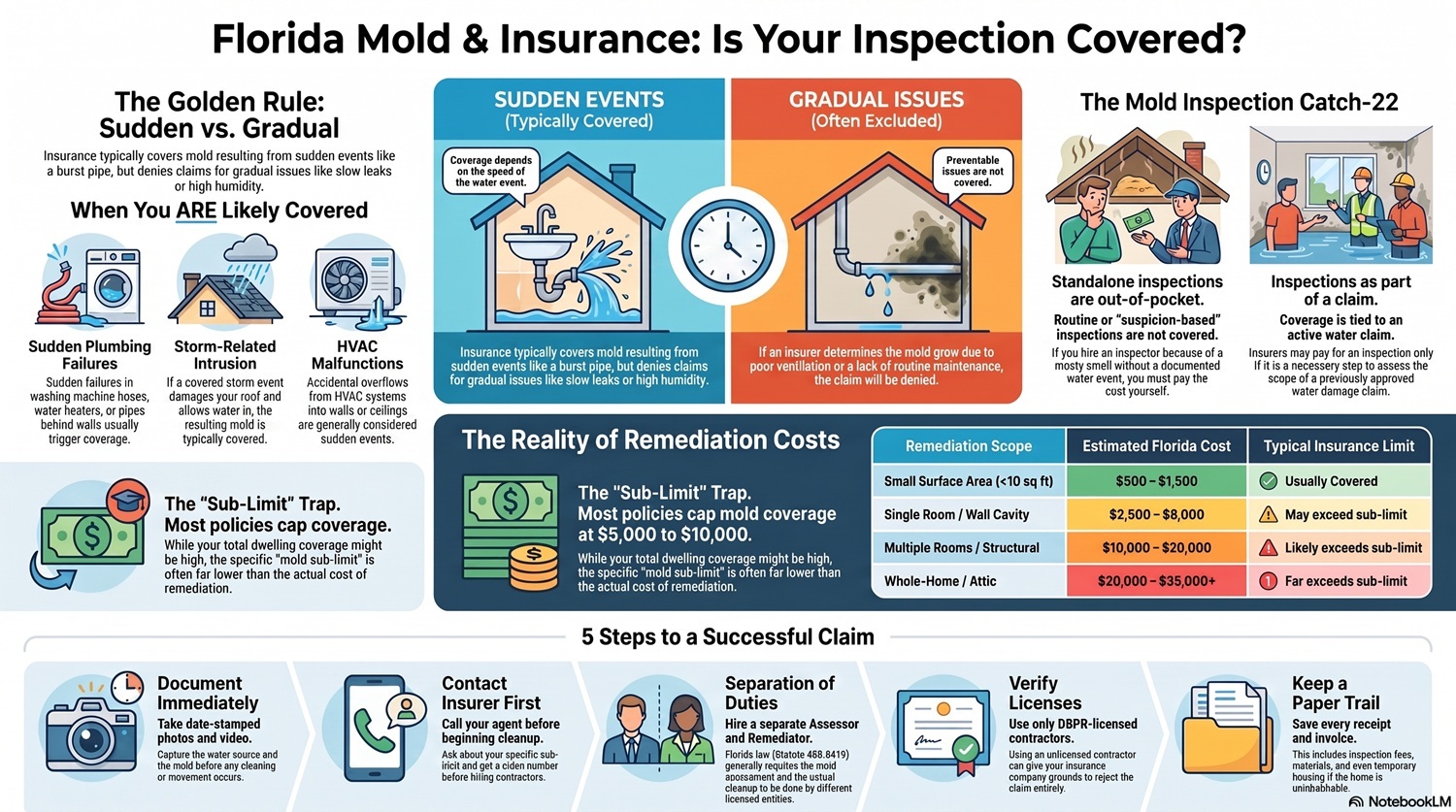

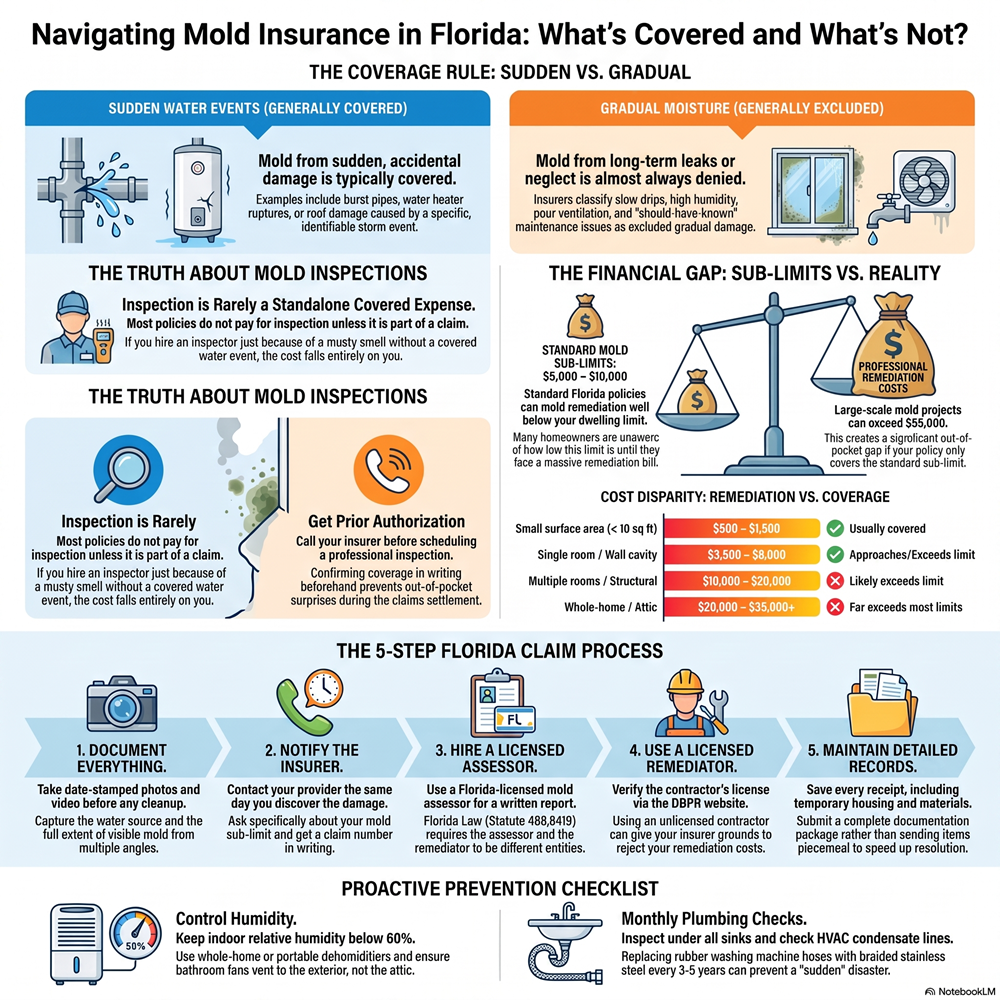

Standard homeowners insurance in Florida may cover mold — but only under specific conditions. If mold develops as a direct result of a covered water damage event, like a burst pipe or a washing machine overflow, your policy may help pay for remediation. If mold develops slowly over time due to a slow leak, high humidity, or poor ventilation, most policies will not cover it. The cause of the moisture is the defining factor.

Why Mold Is a Bigger Problem in Florida Than Most States

Florida consistently ranks among the worst states in the country for mold risk, and it’s not hard to understand why. With average relative humidity levels sitting between 74% and 90% depending on the season, indoor surfaces stay damp enough to support mold growth with very little additional moisture needed. This isn’t a seasonal problem — it’s a year-round reality for Florida homeowners.

Florida’s Humidity Creates Near-Perfect Mold Conditions Year-Round

Mold spores begin colonizing surfaces when relative indoor humidity stays above 60% for extended periods. In Florida, maintaining humidity below that threshold requires active effort — dehumidifiers, properly functioning HVAC systems, and good ventilation habits. When any part of that system fails, or when a weather event introduces additional moisture, mold can establish itself within 24 to 48 hours.

South Florida in particular — Miami-Dade, Broward, and Palm Beach counties — experiences conditions that accelerate mold growth even faster. High overnight temperatures prevent surfaces from drying out, and air conditioning systems that cycle on and off frequently can create condensation inside walls and ductwork, creating hidden mold problems homeowners don’t discover until significant damage has already occurred.

Common Indoor Moisture Sources That Trigger Mold Growth

Outdoor humidity isn’t the only culprit. Inside Florida homes, several common sources introduce moisture that feeds mold growth:

- Burst or leaking plumbing pipes behind walls or under slabs

- Roof leaks following storm damage or missing shingles

- HVAC condensation line clogs causing water overflow into walls or ceilings

- Washing machine hose failures or dishwasher leaks

- Improperly sealed windows and doors allowing rainwater intrusion

- Bathroom exhaust fans venting into attic space instead of outdoors

Many of these sources go undetected for weeks or months. By the time a homeowner spots visible mold, the underlying moisture problem has often been active long enough that insurers may classify it as gradual damage — which changes the coverage picture entirely.

Does Homeowners Insurance Cover Mold Inspection in Florida?

This is one of the most commonly misunderstood aspects of mold-related insurance coverage. The inspection itself — hiring a certified mold inspector to identify whether mold is present and assess its extent — is generally not a standalone covered expense under a standard Florida homeowners policy. Coverage for inspection costs, when it exists at all, is usually tied directly to an active, covered water damage claim.

When Mold Inspection Costs May Be Covered

If a covered water damage event has already been established — say, a pipe burst and water soaked through your walls — your insurer may include mold inspection as part of the broader claims process. In this scenario, the inspection is a necessary step in assessing the full scope of covered damage, and the cost may be rolled into the overall claim settlement. Some policies explicitly include inspection costs within their mold remediation sub-limit coverage.

It’s worth calling your insurer before scheduling an independent mold inspection if you’re hoping to have that cost covered. Getting prior authorization or at minimum confirming coverage in writing protects you from paying out of pocket for an inspection the insurer later refuses to reimburse.

When Mold Inspection Costs Are Typically Not Covered

If you suspect mold but don’t have an active covered claim — perhaps you’ve noticed a musty smell or visible discoloration but haven’t experienced a documented water event — the cost of a professional mold inspection will almost certainly fall on you. Routine inspections, inspections ordered during a home purchase, or inspections prompted by general concerns rather than a specific covered loss are treated as maintenance expenses, not insurance claims.

When Homeowners Insurance Covers Mold Damage in Florida

Coverage comes down to one core question: what caused the water that caused the mold? When the answer is a sudden, accidental event that your policy already covers, mold remediation costs may follow. When the answer involves time, neglect, or gradual buildup, coverage disappears fast.

Sudden Water Damage Events That Typically Trigger Coverage

Florida homeowners policies generally extend mold coverage when mold results directly from these types of sudden water damage events:

- A pipe bursting inside a wall due to pressure failure

- An air conditioning condensate line backing up and overflowing

- A water heater rupturing and flooding an adjacent room

- A washing machine supply hose failing suddenly

- Accidental overflow from a bathtub, sink, or toilet

- Rain entering through a roof damaged by a covered storm event

The key word in every one of these scenarios is sudden. Insurers look for events that happened at a specific, identifiable point in time — not damage that accumulated over weeks or months. If you can point to the day the pipe burst, the night the storm hit, or the moment the appliance failed, you’re in a much stronger position when filing a mold-related claim.

How Coverage Limits Apply to Mold Remediation Costs

Even when mold damage is covered, standard Florida homeowners policies typically apply a sub-limit specifically for mold remediation — meaning the amount available for mold is capped well below your overall dwelling coverage limit. These sub-limits commonly range from $5,000 to $10,000, which sounds like a reasonable amount until you understand what professional mold remediation actually costs in Florida.

A mid-sized mold remediation project in Florida — affecting one bathroom, part of a wall cavity, or a section of HVAC ductwork — can run between $3,500 and $8,000. Larger projects involving multiple rooms, structural materials like drywall and subfloor, or attic remediation can exceed $20,000 to $30,000 easily. When your sub-limit is $5,000 and your remediation bill is $22,000, the gap comes directly out of your pocket.

What Increasing Your Mold Coverage Limit Means for Your Policy

Some Florida insurers offer the option to increase the mold remediation sub-limit as a policy endorsement. This means paying a slightly higher premium in exchange for a higher coverage ceiling on mold-related claims. For Florida homeowners — especially those in high-humidity coastal areas or homes with older plumbing — this endorsement is worth a direct conversation with your insurance agent.

Increasing your mold coverage limit doesn’t change when coverage applies. You still need a qualifying covered water event to trigger a mold claim. What it changes is how much financial protection you have when that event occurs and mold remediation turns out to be more extensive than anticipated.

When Homeowners Insurance Does Not Cover Mold in Florida

Just as important as knowing when coverage applies is knowing exactly when it doesn’t — because the exclusions in mold coverage are broad, and insurers enforce them consistently. Florida’s unique climate means many of the most common mold scenarios fall squarely into excluded territory.

Florida homeowners insurance policies typically exclude mold damage resulting from any condition the homeowner knew about or should have reasonably discovered through normal maintenance. This is a wide standard, and claims adjusters are trained to look for evidence of pre-existing moisture problems — water stains, deteriorating caulk, corroded pipe fittings — that suggest the damage didn’t happen overnight.

Long-Term Leaks and Gradual Moisture Buildup

A slow drip under a bathroom sink, a hairline crack in a supply line, a roof flashing that’s been separating for two rainy seasons — these are the scenarios where mold claims are denied most frequently. Insurers classify these as gradual damage, and virtually every standard homeowners policy in Florida excludes it explicitly. The reasoning is that the homeowner had the opportunity to discover and fix the problem before it escalated into a mold situation.

Poor Ventilation and Maintenance Neglect

Mold that develops because a bathroom fan hasn’t worked in three years, because crawlspace vents were blocked, or because an HVAC filter was never replaced doesn’t qualify as covered damage — it qualifies as a maintenance failure. Florida’s building environment demands active upkeep, and insurers treat inadequate ventilation as the homeowner’s responsibility, not a covered peril. For more information, you can explore when homeowners insurance covers mold.

How to File a Mold-Related Insurance Claim in Florida

If you’ve experienced a covered water event and discovered mold, how you handle the next 48 to 72 hours significantly impacts whether your claim succeeds. Florida’s insurance market is competitive and claim scrutiny is high — moving through the process correctly matters.

The claims process for mold damage isn’t dramatically different from other property damage claims, but mold introduces time pressure that other claims don’t have. Mold spreads. Every hour between discovery and remediation is an hour the damage can expand — and an hour an insurer can later argue you failed to mitigate the loss.

1. Document the Water Damage and Mold Growth Immediately

Before anything is moved, cleaned, or dried, take extensive photos and video of the water source, the affected area, and any visible mold growth. Date-stamp everything. Capture the full context — not just close-ups of mold but wide shots showing the room layout, proximity to plumbing, and overall damage scope.

Write down the timeline: when you first noticed water, when you discovered mold, and what immediate steps you took. This contemporaneous record becomes critical if the insurer questions when the damage occurred or whether you acted promptly to stop it from spreading.

2. Contact Your Insurance Provider Before Any Cleanup Begins

Notify your insurer as soon as possible after discovery — ideally the same day. Most Florida homeowners policies require prompt notification of a loss, and delaying that call gives the insurer grounds to question your claim. Ask specifically about mold coverage, your applicable sub-limit, and whether you need pre-authorization before hiring any remediation contractors. Get the claim number in writing before you proceed.

3. Get a Professional Mold Inspection and Written Report

Hire a Florida-licensed mold assessor — separate from any remediation company, as Florida law requires the assessment and remediation to be performed by different entities under Florida Statute 468.8419 unless visible mold is less than 10 sq ft or the remediation is performed 12 months after the assessment. The written mold assessment report documents the type, location, and extent of mold growth and becomes the foundation of your insurance claim. Without it, you’re negotiating blind.

4. Work With a Licensed Florida Mold Remediation Contractor

Florida requires mold remediators to hold a state license under the Department of Business and Professional Regulation (DBPR). Working with an unlicensed contractor doesn’t just risk poor results — it can give your insurer grounds to reject remediation costs entirely. Verify the contractor’s license at the DBPR website before signing any contract.

Get a written remediation protocol based on the mold assessor’s report before work begins. This protocol outlines exactly what work will be done, what containment methods will be used, and what clearance testing will confirm successful remediation. Having this document protects you if the insurer questions whether the scope of work was necessary.

5. Keep All Receipts and Records for Your Claim

Every dollar you spend related to the mold event — inspection fees, temporary housing if the home is uninhabitable, remediation costs, reconstruction materials — should be documented with receipts and invoices. Organize these chronologically and keep both digital and physical copies.

Submit a complete documentation package to your insurer rather than sending items piecemeal. A well-organized claim submission signals that you’re a prepared, informed policyholder — and it reduces the back-and-forth that can slow claim resolution by weeks.

If your insurer disputes the scope of damage or offers a settlement that doesn’t reflect the actual remediation cost, you have options. Florida homeowners have the right to invoke the appraisal process outlined in their policy, hire a licensed public adjuster to represent their interests, or file a complaint with the Florida Department of Financial Services.

How to Prevent Mold and Protect Your Insurance Coverage

Prevention is the most reliable mold strategy a Florida homeowner has — and it also happens to protect your insurance standing. Insurers look for evidence of maintenance neglect when evaluating mold claims, so a documented habit of proactive upkeep can be the difference between a covered claim and a denied one. For more information, you can explore when homeowners insurance covers mold.

The goal isn’t a mold-free home, which is unrealistic in Florida’s climate. The goal is eliminating the controllable moisture sources that give mold the opportunity to establish itself before you ever know it’s there.

Fix Plumbing Leaks the Moment You Spot Them

A dripping faucet or a slightly damp cabinet floor under the kitchen sink might feel like a minor inconvenience, but in Florida’s humidity, it’s a mold incubator. The moment you spot any sign of moisture where it shouldn’t be — water stains on ceilings, soft spots in flooring, unexplained increases in your water bill — treat it as urgent.

Document every repair you make. Keep invoices from licensed plumbers, photos of the completed repair, and dates of service. This paper trail demonstrates to any future claims adjuster that you actively maintained your home and addressed issues promptly — which directly supports a covered mold claim if one ever arises from a sudden event rather than neglect.

- Inspect under all sinks monthly for moisture, discoloration, or soft cabinet flooring

- Check washing machine supply hoses annually and replace rubber hoses with braided stainless steel versions every 3 to 5 years

- Have your HVAC condensate drain line cleared at least once per year — more often in South Florida

- Inspect your roof flashing, seals around skylights, and attic ventilation after every major storm

- Test your water heater pressure relief valve annually and replace the unit if it’s older than 10 years

Every one of these maintenance steps does double duty — it reduces your actual mold risk and builds the documented maintenance history that supports insurance claims when sudden water events do occur.

Control Indoor Humidity With Dehumidifiers and Proper Ventilation

Keeping indoor relative humidity below 60% is the single most effective mold prevention measure available to Florida homeowners. A whole-home dehumidifier integrated into your HVAC system is the most efficient approach for larger homes, while portable units like the Frigidaire FFAD7033R1 — rated for spaces up to 1,500 square feet — handle targeted areas like bathrooms, laundry rooms, or bonus rooms effectively.

Ventilation matters just as much as dehumidification. Bathroom exhaust fans must vent directly to the exterior of the home — not into the attic, which is a common installation error that turns the attic into a mold zone. Run exhaust fans for at least 20 minutes after every shower, check that kitchen range hoods are functioning and vented properly, and ensure your attic has adequate soffit and ridge vent coverage to prevent heat and moisture from accumulating above your living space.

Review Your Policy Limits Before Mold Costs Catch You Off Guard

Pull out your current homeowners policy and look specifically for the mold, fungus, and wet rot sub-limit — not your overall dwelling coverage, but the specific cap on mold remediation. If that number is $5,000 or $10,000 and you live in a home with older plumbing, a flat roof, or a crawlspace, call your agent this week and ask what it would cost to increase it. In Florida’s remediation market, that conversation could save you $15,000 or more on a single claim.

Frequently Asked Questions

Florida homeowners ask the same mold coverage questions repeatedly — and with good reason. The answers aren’t always straightforward, and the financial stakes are high enough that getting them wrong costs real money.

Does homeowners insurance cover mold inspection costs in Florida?

Mold inspection costs are generally not covered as a standalone expense under a standard Florida homeowners policy. If the inspection is part of an active, covered water damage claim, costs may be included within the mold remediation sub-limit. Always contact your insurer before scheduling an independent inspection if you intend to seek reimbursement — getting verbal or written confirmation upfront prevents disputes after the fact.

What types of mold damage are typically excluded from Florida homeowners insurance?

Most Florida homeowners policies exclude mold damage that results from long-term moisture problems, gradual leaks, flood water intrusion, poor ventilation, and general maintenance neglect. Mold that develops following an excluded water source — including rising floodwater from storms, which requires separate flood insurance through the National Flood Insurance Program (NFIP) — is not covered under a standard homeowners policy regardless of how severe the mold damage becomes.

How much does mold remediation cost in Florida without insurance coverage?

Without insurance coverage, Florida homeowners pay for mold remediation entirely out of pocket — and costs vary significantly based on the size of the affected area, the type of mold present, and how deeply the mold has penetrated building materials.

Small surface mold issues confined to tile grout or a small section of drywall may cost $500 to $1,500 to remediate professionally. Mid-range projects — a bathroom wall cavity, a section of HVAC ductwork, or mold beneath flooring in a single room — typically run $3,500 to $8,000. Large-scale remediation involving multiple rooms, structural framing, or attic spaces can reach $20,000 to $35,000 or more.

These costs don’t include post-remediation reconstruction — replacing drywall, flooring, insulation, or cabinetry — which adds another layer of expense on top of the remediation itself.

Remediation Scope Estimated Cost (Florida) Typical Coverage Sub-Limit Small surface area (under 10 sq ft) $500 – $1,500 May be covered within sub-limit Single room / wall cavity $3,500 – $8,000 May approach or exceed sub-limit Multiple rooms / structural materials $10,000 – $20,000 Likely exceeds standard sub-limit Whole-home / attic remediation $20,000 – $35,000+ Far exceeds most sub-limits

These figures underscore why understanding your policy’s mold sub-limit before a loss occurs — not after — is one of the most financially important things a Florida homeowner can do.

Can I add extra mold coverage to my existing Florida homeowners policy?

Yes, many Florida insurers offer endorsements that increase the mold remediation sub-limit beyond the standard amount included in your base policy. The availability and cost of these endorsements varies by insurer and by the age, location, and construction type of your home. This is a conversation worth having directly with your agent, particularly if your home has older plumbing, a flat or low-slope roof, or any history of water intrusion. A modest premium increase for higher mold coverage is almost always worth it in Florida’s climate.

What should I do if my insurance company denies my mold damage claim in Florida?

A denied mold claim is not necessarily a final answer. Florida homeowners have several concrete options for challenging a denial, and using them strategically often results in a different outcome.

Start by requesting the denial in writing if you haven’t already received it. The denial letter must specify the exact policy language or exclusion the insurer is relying on. Read that language carefully against the facts of your specific situation — adjusters sometimes apply exclusions too broadly, and a well-documented claim with a clear sudden-event timeline can overcome a denial that initially seemed firm.

If you believe the denial is incorrect or the settlement offer is unreasonably low, consider these steps:

- File a written complaint with the Florida Department of Financial Services (DFS) at myfloridacfo.com — DFS has authority to investigate insurer conduct and mediate disputes

- Hire a licensed Florida public adjuster to re-evaluate the claim on your behalf — public adjusters work on contingency and are experienced at identifying documentation gaps that support a stronger claim

- Invoke the appraisal clause in your policy if the dispute is about the dollar amount of covered damage rather than whether coverage applies — this process brings in neutral appraisers to establish the loss value

- Consult a Florida property insurance attorney if the denial involves bad faith claim handling — Florida has specific statutes governing insurer conduct and remedies for policyholders when those standards aren’t met

Time limits matter in the dispute process. Florida law sets deadlines for filing suit against an insurer, and waiting too long to challenge a denial can forfeit your legal options entirely. If you’re considering formal action, consult an attorney sooner rather than later.

Mold claims are among the most contested in Florida’s insurance market — but they’re also among the most winnable when homeowners have thorough documentation, a clear event timeline, and a full understanding of their policy rights.

3 Replies to “Does Homeowners Insurance Cover Mold Inspection in Florida?”